After 10 consecutive months of rising output, January saw UK construction fall back.

Shrinking order books and rising cost pressures contributed to the weakest business activity expectations since October 2023, according to purchasing managers.

At 48.1 in January, down significantly from 53.3 in December, the headline seasonally adjusted S&P Global UK Construction Purchasing Managers’ Index (PMI) registered below the 50.0 no-change threshold for the first time since February 2024. (Anything above 50.0 indicate growth; below indicates dwindling output.)

Construction companies cited delayed decision-making by clients on major projects and general economic uncertainty had weighed on business activity at the start of 2025. A number of firms also commented on the impact of subdued market conditions in the residential building sector.

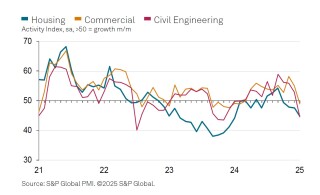

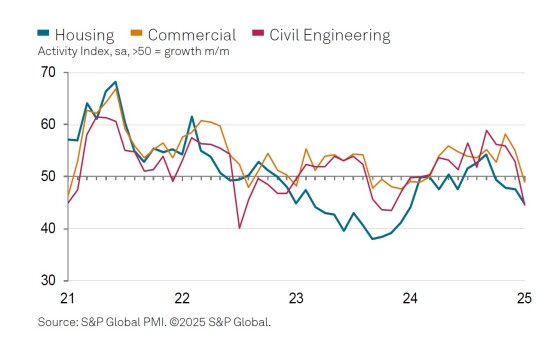

All three broad sectors of the industry moved into negative territory in January. House-building (index at 44.9) decreased for the fourth successive month and at the fastest pace since January 2024. Civil engineering activity (44.6) declined at a relatively sharp rate, although this partly reflected disruptions from unusually wet weather at the start of the year. Commercial construction category also returned to contraction in January (48.9). This was linked to a lack of tender opportunities and a reluctance among clients to commit to new projects.

January data pointed to a decline in incoming new work for the first time in 12 months. Although only modest, the rate of contraction was the steepest since November 2023. Anecdotal evidence suggested that a lack of confidence among clients and worries about the UK economic outlook had contributed to fewer sales enquiries.

Purchasing activity decreased for the second month in a row, reflecting weak order books and a lack of new work to replace completed projects. Despite softer demand for construction products and materials, the latest survey indicated the steepest rise in input costs since April 2023. Construction companies noted that suppliers had sought to pass on rising energy, transportation and staff costs. Moreover, vendor performance deteriorated to the greatest extent for two years, which was partly linked to shipping delays.

Tim Moore, economics director at S&P Global Market Intelligence, which complies the monthly survey, said: “UK construction output fell for the first time in nearly a year as gloomy economic prospects, elevated borrowing costs and weak client confidence resulted in subdued workloads.

“Output levels decreased across the board in January, with particularly sharp reductions seen in the residential and civil engineering categories.

“Construction firms noted the fastest fall in residential work for 12 months as market conditions remained somewhat subdued. Anecdotal evidence suggested that caution regarding demand for new projects was prevalent at the start of 2025, despite strong policy support for house-building and hopes for a longer-term boost to supply via planning reform.

“The forward-looking survey indicators were also relatively downbeat in January. New orders decreased at the fastest pace since November 2023 amid many reports of delayed decision-making by clients. Reduced workloads, combined with concerns about the general UK economic outlook, led to a dip in business activity expectations to the lowest for 15 months.

“There was little respite on the supply front, as transport delays meant that vendor lead times lengthened to the greatest extent for two years. Demand for construction items softened again in January, but purchase price inflation was the highest since April 2023 as suppliers sought to pass on rising energy, fuel and wage costs.”

Brian Smith, head of cost management and commercial at Aecom, commented: “A winter slowdown is unsurprising given the broader economic mood but confidence will need to improve quickly if the sector is to regain some of 2024’s momentum and deliver on the government’s growth agenda.

“After a sobering start to 2025, firms will be hoping to see further cuts to interest rates that encourage clients to green-light projects and unleash more private investment throughout the year.

“That said, contractors’ growth prospects are good this year, with pipelines suggesting there is sufficient work to go around. The speed of delivery though could be challenged their willingness to take on significant amounts of new work given the volatility of recent years and long-standing challenges around labour availability.”

Terry Woodley, managing director of development finance at money lender Shawbrook, said: “The adverse weather put a definite dampener on activity this month, with construction output dipping, as well as the continued declines in areas such as civil engineering. Not all has been lost, however, as developers have responded positively to the Chancellor’s recent speech on growth in which she outlined the next steps in streamlining planning decisions to ensure the 1.5 million new homes target is met.

“Though a welcome update, there are still concerns around the current skills shortage in the sector, which could stand in the way of Labour’s vision of ‘shovels in the ground and cranes in the sky’. Construction activity has the potential to take off this year, but until these issues are addressed, the sector risks being held back.”

Atul Kariya, head of real estate and construction at accountancy group MHA, said: “It is hardly surprising that construction PMI activity has fallen as the industry and the economy as a whole are now starting to see the full impact of the proposed tax rises and increased labour costs in the autumn budget. These are starting to feed through into overall business sentiment in the sector as well as ongoing challenging economic conditions in the UK and overseas. The glimmers of optimism that the industry witnessed in September last year when the PMI soared to 57.2 now seem a little distant, despite order book and enquiry levels remaining relatively buoyant.

“Even though there has been a recent an increase in house sales this is most likely to have been driven by the impending increase in stamp duty in April which is reflected in share values across the sector as housebuilders are currently trading even lower than they did during the pandemic.

“The housebuilding sector has witnessed a sharp decline despite the government’s planning reforms on housing that are due to be kickstarted in the spring, while commercial construction also saw a decline in output as nervousness remains around the UK’s economic growth.

“While the short term outlook remains gloomy we are hopeful that with successive cuts in interest rates throughout 2025, anticipated to start today, there will be a pickup in activity and optimism in the sector.”

Got a story? Email news@theconstructionindex.co.uk

#Construction #PMI #slumps #negative