KanawatTH

Performance

During the first quarter of 2025, Night Watch Investment Management LP depreciated by -2.11% net of fees.

|

Night Watch Investment Partners LP – Net Performance Since Inception (in USD) |

|||||||||||||

|

Jan |

Feb |

Mar |

Apr |

May |

Jun |

Jul |

Aug |

Sep |

Oct |

Nov |

Dec |

Year |

|

|

2025 |

2.56% |

-0.45% |

-4.12% |

-2.11% |

|||||||||

|

2024 |

-0.82% |

0.58% |

7.09% |

-0.24% |

5.14% |

-5.20% |

9.11% |

-0.23% |

-1.34% |

-2.40% |

2.10% |

-2.92% |

10.30% |

Elevated levels of market volatility continued during Q1. US stocks underperformed their international peers. Our portfolio was largely immune from the market volatility during Q1 due to our international diversification, as well as some stock-specific investments that continue to work.

Our largest contributors to performance were Haypp, Marex (MRX), Mr. Cooper (COOP) and Brookdale Senior Living (BKD). Our biggest detractors were Distribution Solutions Group (DSGR), X-Fab Silicon Foundries (OTCPK:XFABF) and AAR Corp (AIR), which were impacted by overall market volatility but still hold strong investment theses in the long run.

Portfolio

Night Watch manages a global value strategy that differentiates on the following points:

Catalyst – We predominantly buy value companies with an identifiable catalyst for a rerating. Catalysts can include industry tailwinds or company specific catalysts (e.g., earnings inflection, CEO changes, refinancing).

Inside Ownership – We aim to find companies where management has considerable ownership in the company. We consider this alignment of interest to be an important determinant of share price performance.

Unique Names – To differentiate from a long list of other value strategies, we seek unique portfolio holdings that have little overlap with a typical wealth management portfolio. We thus aim to provide our LPs with diversification from their other investments in addition to strong performance.

The portfolio as of March 31 st, 2025 is as follows:

|

Theme |

Weight |

Positions |

Insider Ownership |

Catalyst |

|

Housing |

15.2% |

4 |

1/4 |

3/4 |

|

Consumer |

11.6% |

3 |

3/3 |

2/3 |

|

Aerospace |

10.6% |

2 |

2/2 |

2/2 |

|

Counter-Cyclicals |

8.5% |

1 |

1/1 |

1/1 |

|

Energy / Mineral Drilling |

9.0% |

4 |

1/4 |

4/4 |

|

US Onshoring/ Fiscal Stimulus |

9.7% |

1 |

1/1 |

1/1 |

|

Chinese Consumer |

12.8% |

4 |

2/4 |

2/4 |

|

Europe – Quality names for value price |

37.7% |

10 |

6/10 |

10/10 |

|

Event Driven/ Other |

0% |

|||

|

Funding Shorts |

-9.7% |

|||

|

Cash |

-5.5% |

|||

|

Total |

100% |

29 |

17/29 |

26/29 |

Largest positions:

- Distribution Solutions Group (9.7%)

- Marex (8.5%)

- Allfunds (7.9%)

- Haypp (7.4%)

- AAR Corp (7.1%)

Strategy Update

In previous quarters we presented our portfolio in terms of various themes to which we are seeking exposure. Those themes remain relevant, but in this letter, we want to dive deeper into the strategy behind our global diversification. In broad terms, we have a basket with US stocks, European stocks and Hong Kong-listed stocks.

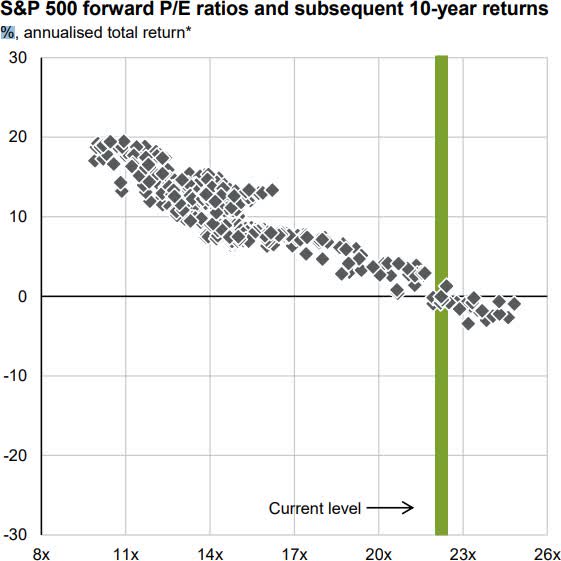

USA

The S&P500 (SP500, SPX) is the most expensive developed market globally. At a P/E multiple of 21.3x, it trades roughly 1.5 standard deviations above its 20 year mean. The following graph shows the expected future return per year over the subsequent 10-year, as a function of P/E multiple. If history is any guide, S&P500 investors should expect to earn anywhere between -1% to 3% per year for the next 10 years.

Fortunately, there are many US small and mid-caps that trade at reasonable valuations and have improving businesses as well as good management teams. This is where we focus our attention.

The high valuations in the US for the last years were justified by higher economic growth compared to the rest of the world. This seems to be changing.

The new Trump administration is expected to make various policy changes that are negative for stocks, such as the introduction of tariffs and a decrease in government spending. At the same time, it promises policy changes that could boost stock prices such as deregulation, corporate tax cuts and fiscal stimulus. During

February and March, the administration’s focus was on the negative policy changes. More importantly, there is a great amount of uncertainty around his policies. Tariffs seem to be introduced and then cancelled at will, which negatively impacts consumer confidence as well as business confidence. Nobody will invest in a new car factory based on newly introduced tariffs on imported cars, if those tariffs can be cancelled a week later.

As a consequence, we have exited the most GDP sensitive businesses during the quarter. For instance, in our Q4 letter, we mentioned our investment in United Airlines (UAL). Our thesis was based on improving supply- demand dynamics within the US aviation market. After the first signs of travel bans for various government employees, we completely exited this position at a very good return for our investors.

We added significantly to our position in Distribution Solutions Group (DSGR), Mr. Cooper (COOP), AAR Corp (AIR) and DraftKings (DKNG). For all those investments, we expect significant earnings growth regardless of macro-economic conditions. They benefit from large inside ownership and have a track record of superior execution. They are our sleep-well names during volatile times.

Europe

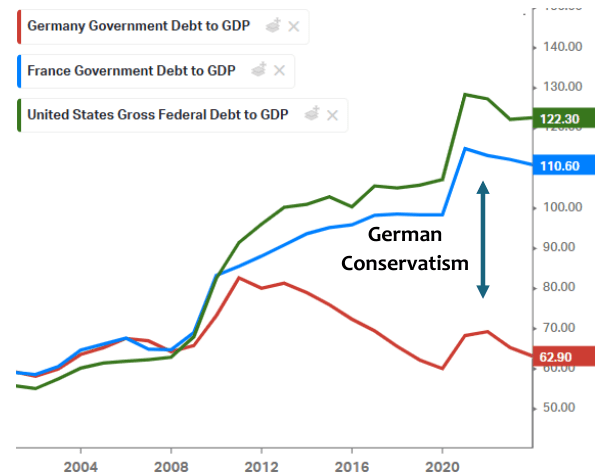

During Q1, the German stock market appreciated by 18% after the Germans realized their economy has been held back by their fiscal discipline ever since the Great Financial Crisis. This was supplemented by the sudden belief in Europe that they have to invest more into their national defense. Increased government spending directly supports GDP growth which is supportive for European stocks. The market celebrated by buying into the DAX ETF, the main German index.

However, in typical European fashion, we expect the current spending plans to be watered down, and implementation to take longer than currently anticipated. Furthermore, some of the largest DAX constituents are SAP, Deutsche Telekom and Allianz, which are not necessarily the companies that will benefit the most from any fiscal spending. They’re also all inefficient conglomerates with poor historic track records of value creation.

Our European strategy has always been to focus on the small number of entrepreneurial companies with a clear future strategy. We avoid conglomerates.

We want our CEOs to dream about creating shareholder value. And when they succeed, we want them to become rich in the process. The average CEO of a European conglomerate dreams about stakeholders, but only between the hours of 9 to 5. That’s why our focus in Europe is even more on the management team and their alignment of interests. We prefer management teams who have coinvested with their shareholders and who stand to become extremely rich – but only if we get rich too.

Our largest positions in Europe remain Allfunds (ALLFG NA) and Haypp (HAYPP SS), both of which have been discussed in previous updates. As a reminder, Haypp is the dominant e-commerce platform for nicotine pouches such as Zyn. During Q4, various regulatory risks materialized at once. Despite those headwinds, and contrary to everyone’s expectations, Haypp reported its strongest quarter ever in Q4. Haypp’s business benefits from a more diverse customer base, and the dominance of Zyn was a net negative. Since last quarter, various new competing products to Zyn have come to market such as Velo Plus and Alp, and Haypp likely stands to benefit further. The magnitude of the improvement in profitability came as a surprise to us. We believe last quarter underscores the quality of both Haypp’s business model, as well as of its management team.

We are currently on our way to Sweden to attend Haypp’s Investor Day on April 3 rd and to learn more about their strategy for the next few years.

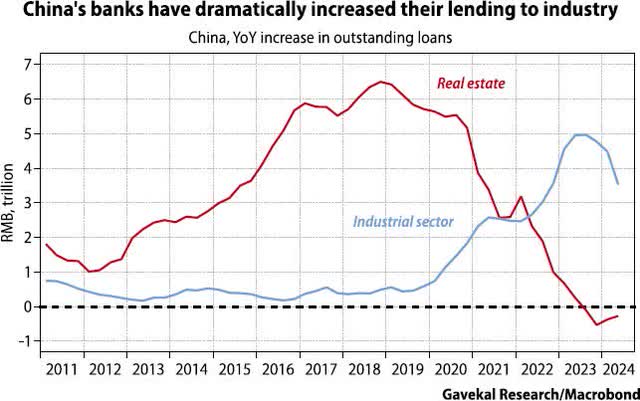

China

China has long been one of the cheapest markets in the world. China has gone through 5 years of deflation of its property bubble, which has caused most global investors to look elsewhere. What has largely gone unnoticed is the major transition the Chinese economy has undergone. The Chinese economy is no longer driven by the construction of ‘ghost towns’ or ‘bridges to nowhere’. Instead, the economy is driven by EV exports to Latin America, or the export of high-speed trains to Indonesia. This is best illustrated in the graph by our friends from Gavekal Research.

Since October 2024, China has introduced various measures to stimulate its domestic economy, such as subsidies when you trade in your phone or car. Such measures could take a while before they start impacting consumer confidence, but we believe that consumer spending has bottomed and 2025 will show a return to growth. Boosting the stock market also seems a clear priority. The CCP has introduced policies that allow national insurance companies to invest more in equities, and corporations can now borrow from local state banks to do buybacks. If Xi Jinping wants stock prices to go up, we want to own those stocks. Our focus remains on the Chinese consumer sector, as well as on companies that actively return capital to shareholders.

Investment Thesis: DPC Dash

Our largest Hong Kong listed investment is currently DPC Dash (OTCPK:DPCDF, 1405 HK), who owns the exclusive rights to operate Domino’s Pizza franchises in China, Hong Kong and Macau. We met with their management and 2 board members at the ICR conference in Orlando this January.

When I briefly lived in Beijing in 2008, the most popular Western pizza joint was Pizza Hut (owned by Yum China). At the time, Domino’s was largely absent in the Chinese market. This was because unlike Yum, Domino’s Pizza had never wanted to invest equity in its Chinese growth, preferring to rely fully on the franchise model. Therefore, Domino’s lacked the funding to hit critical mass and brand awareness.

This changed around 2017 when a new, local management team was hired and the parent Domino’s Pizza provided capital for expansion. DPC Dash has since grown to 1,000 stores. Importantly, since they exceeded the critical level of ~500 stores in 2021, they seem to have critical mass which results in the required brand awareness. Store count is currently growing 30 to 35% per year. The new management has localized the food offering (Durian Pizza) and to put it simply: Domino’s is hot in China. Several of the new stores have queues of up to 4 hours during their grand opening. New stores are often so overwhelmed by demand that they don’t do pizza deliveries in the first couple of months.

Let’s look at some simple math. A store costs roughly $200k to open. The average store does $100k in operating profit, meaning the payback is 2 years on average. However, when entering new cities, DPC has reported payback periods of less than a year. Companies that can reinvest capital at 50-100% ROIC are rare. We believe there is even some upside to the per-store profitability as DPC continues to grow and they will reap more scale benefits.

We bought our shares at a valuation of roughly $1.2m per store, or 12x store-level EBIT if we ignore corporate overhead. There are 5 other publicly traded Domino’s franchises. The worst performers (Poland, Saudi Arabia) trade at a valuation of $750k per store, but these geographies show no profitability (Poland) or negative growth (Saudi). The highest valuations are seen in India, where the valuation is $1.7m per store, even though Indian stores do half as much in revenue as Chinese stores and growth is significantly less.

More importantly, we see a realistic pathway for DPC Dash to grow from 1,000 stores in 2024 to 2,000 stores in 2027 and 3,000 stores in 2029, all organically funded. We believe 3,000 stores is achievable given that Pizza Hut owns roughly 3,600 stores and is still growing at 10%. This would bring the valuation down to $400k / store if we are willing to look out 5 years. By this simple math, DPC Dash has 3x to 5x potential if it continues to execute.

Conclusion

While the US economy is slowing and valuations are at high levels, both China and Europe are increasingly stimulating their economies and valuations are a lot more attractive. We believe our diversified exposure to the 3 regions provides meaningful downside protection in volatile times.

We intend to keep adding unique and attractive names to our portfolio. We are currently travelling to Sweden and Israel to meet with our existing portfolio holdings, as well as to source new investment ideas.

On behalf of the Night Watch team,

Roderick van Zuylen | Chief Investment Officer

Eileen Ke | Chief Operating Officer

|

Important Disclosures This document was prepared by Night Watch Investment Management, LLC (“NWIM”) on December 6th, 2023, based on information available as of December 6th, 2023, and is subject to amendment. The information and opinions contained in this document (including information obtained from third-party sources) are for background purposes only and do not purport to be full or complete, and do not in any way constitute personalized investment advice or an investment recommendation on the part of NWIM. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document, and no liability is accepted as to the accuracy or completeness of any such information or opinions. All investments involve the risk of a loss of capital. NWIM believes that its proprietary investment program, research and risk-management techniques moderate this risk through the careful selection of portfolio investments. However, no guarantee or representation is made that NWIM’s investment program will be successful, and investment results may vary substantially over time. Past performance is not a guide to future performance. This publication makes no recommendations whatsoever regarding buying, selling, or holding any specific security, class of securities, or securities of a class of issuers. You are required to conduct your own due diligence, analyses, draw your own conclusions, and make your own investment decisions. Commentary is provided without reference to any investment strategy or product offered by NWIM. NWIM or entities managed by NWIM may be invested in any of the industries or securities mentioned. They may trade in and out of those positions without providing any updates. Certain information contained in this document constitute “forward- looking statements,” which can be identified by the use of certain terminology, such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or other variations thereon or comparable terminology. Any projections or other estimates in this document, including estimates of returns or performance, are “forward- looking statements” and are based upon certain assumptions that may change. Due to various risks and uncertainties, actual events or results, or the actual performance of any investment vehicle, portfolio or product described herein may differ materially from those reflected or contemplated in the forward-looking statements. Actual events are difficult to project and often depend upon factors that are beyond the control of NWIM. TO THE FULL EXTENT PERMITTED BY LAW NEITHER, NWIM NOR ANY OF ITS AFFILIATES, NOR ANY OTHER PERSON OR COMPANY, ACCEPTS ANY LIABILITY WHATSOEVER FOR ANY DIRECT, INDIRECT, OR CONSEQUENTIAL LOSS ARISING FROM, OR IN CONNECTION WITH, ANY USE OF THIS PUBLICATION OR THE INFORMATION CONTAINED HEREIN. NWIM AND ITS AFFILIATES EXPRESSLY DISCLAIM ANY GUARANTEES, INCLUDING, BUT NOT LIMITED TO, FUTURE PERFORMANCE OR RETURNS. Copyright 2025 Night Watch Investment Management, LLC. All rights reserved. |

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

#Night #Watch #Investment #Management #Investor #Letter